As someone in their 30s, it can often be difficult to remind myself about the importance of saving for retirement. After all, imagining myself more than double the age I am now seems like an eternity away. But if thoughts of living out my days penniless don’t inspire me to start saving, I’ve found that the promise of a nice tax break now certainly will.

If you hadn’t noticed, the U.S. tax code isn’t simply designed to cover necessary government functions but is also arranged in such a way as to promote certain behaviors on our part. Case in point: contributing to a retirement account can often have a positive impact on your tax bill. Heck, in some cases, they even let you make contributions up until the last minute to try to entice you further — and this year you’ll even have an extra month to get it done. On that note, let’s take a look at a few different retirement account options and their potential tax time benefits.

401(k)

Starting with one of the most popular retirement savings options, 401(k)s are typically offered through your employer and your contributions are usually a percentage of your earnings. There are several reasons why these accounts are so popular, starting with the basic fact that employers will ask you to join them. Quite honestly, this push and reminder that you should be preparing for retirement can go a long way — as evidenced by their usage.

Of course, there are many other perks to 401(k)s as well. For example, some employers will actually match at least a portion of your contributions and even offer plan participants some form of profit sharing. Another benefit is that your contributions are tax-advantaged, meaning that those funds will be deducted from your taxable income. Finally, contributing to a 401(k) is easy as the funds will automatically be deducted from the paychecks.

Unfortunately, because 401(k) contributions come via payroll, there’s not a way to make additional contributions in a bid to lower your 2020 tax bill. That said, you can always up your contribution percentage going forward — at least until you hit the limit (currently $19,500 a year for tax year 2021). Moreover, even if you do end up hitting that limit, you can still open and contribute to an IRA as well.

Traditional IRA

Next on the list of most popular retirement savings options are individual retirement arrangements/accounts — better known as IRAs. These accounts come in many forms (as you’ll see), but for the purposes of this section, we’ll be talking about traditional IRAs that just about anyone can take advantage of. However, even after that stipulation, there are still plenty of different ways to invest using a traditional IRA.

What’s great about IRAs is that you can either take an active role in how your money is invested or assume a more passive position akin to how your 401(k) is likely managed. For example, for those who want to just contribute and have their investments managed for them, mutual funds or ETFs are the perfect investment vehicle for your IRA funds. Meanwhile, self-directed IRAs give account holders far more investment options, including peer to peer lending, real estate, businesses, or even cryptocurrencies — all at your own risk, of course. Regardless of which route you choose, these funds are also tax-advantaged just like 401(k)s.

Speaking of tax benefits, the cool thing about IRAs is that you can actually make contributions up until tax day — the odd date of May 17th for 2021 — and apply them toward the previous year. This means you could conceivably lower your looming tax bill by making a last-minute contribution to your retirement savings. It should be noted, however, that the annual contribution limit for IRAs is far lower than with 401(ks). For 2020 and 2021, the limit for those under 50 years old is $6,000 while those over 50 can contribute $7,000 a year.

Roth IRA

You know all those benefits we just discussed in regards to IRAs? Well, they all apply to Roth IRAs as well — except for one key part. Instead of your contributions being deducted from your taxable income like with a traditional IRA, Roth IRA holders pay taxes on contributions upfront. That might not sound like a good deal, but it also means that, when it’s time to retire, you can enjoy tax-free distributions from your account. As a result, if you can afford to pay the taxes now and you’re currently in a low tax bracket, it may be worth looking into a Roth IRA instead of a traditional one.

It should also be noted that income limits put restrictions on who is eligible to contribute to a Roth IRA. For tax year 2020, these income limits (based on your modified adjusted gross income) are $139,00 for individual filers and $206,000 for married couples filing jointly. In 2021, they will increase to $140,000 and $208,000 respectively. However, as you approach these limits, the amount you can contribute begins to phase out. This can get a bit complicated, so I’d recommend checking the IRS’s website for the formula used to calculate your contribution limit.

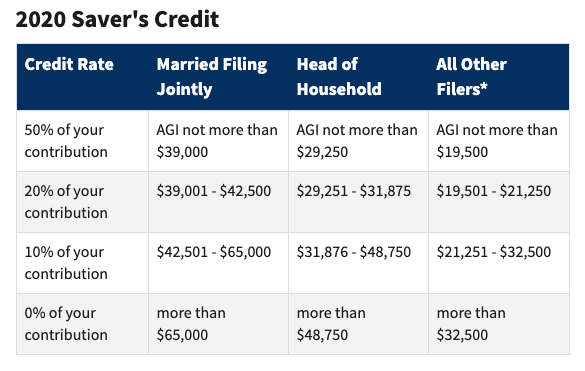

Since you’re paying tax on your Roth IRA contributions upfront, there’s technically not a tax-time benefit to making last-minute contributions in most cases. However, if you earn less than a certain amount of money each year, you could still qualify for what’s called the saver’s credit. This amazing benefit could reduce your tax bill by up to $1,000 ($2,000 if you’re married and filing jointly) by crediting you up to 50% of your contributions to a 401(k), traditional IRA, Roth IRA, or select other accounts. That said, these credits only apply up to the amount of taxes you owe. So, if your total tax liability for the year is $700 and you qualify for a $1,000 Saver’s Credit, the benefit would be maxed at $700 and you’d owe $0 instead of receiving the other $300 back.

These credits are determined by your contributions up to $2,000 ($4,000 for married couples filing jointly) as well as your adjusted gross income (AGI). Here’s a look at the Saver’s Credit benefits for tax years 2020 and 2021:

As you can see, this credit could make a big difference to your tax bill and is even more reason to contribute to your traditional or Roth IRA before April 15th in most years or May 17th for 2021.

SEP IRA

Now that we’ve covered the three biggies in the world of retirement savings accounts, I wanted to cover some lesser-known but potentially beneficial options. Among these are SEP-IRAs (SEP stands for “Simplified Employee Pension” Plan), which hold some important benefits for small business owners and other self-employed individuals.

As you may have already realized, the $6,000 annual contribution limit that most IRAs carry isn’t very high and pales in comparison to the more than $19,500 in contributions 401(k)s allow. That’s where SEP-IRAs come in, boasting a contribution limit that (in most cases) puts the other options to shame. For tax year 2020, SEP-IRA holders are able to contribute up to 25% of their salary or up to $57,000 — whichever is less. This limit is also increasing to up to $58,000 for tax year 2021.

Obviously SEP-IRAs could be a great option for self-employed workers who want to save heavily for their retirement, but there are some downsides to small business owners. For one, SEP rules require business owners to contribute the same percentage of compensation to all of their employees. So, if you elect to set aside 7% of your earnings in a SEP-IRA, you must also contribute 7% of each of your eligible employees’ compensation. Additionally, each employee is 100% vested in their SEP-IRA money at all times. Still, if you only have a few employees, this could be a smart route for your business to go in.

SIMPLE IRA

Lastly, we come to the so-called SIMPLE IRA. In this case, SIMPLE stands for “Savings Incentive Match Plan for Employees,” with the ‘L’ also coming from “Plan” to complete the acronym. Like its description implies, a big difference between a SEP-IRA and a SIMPLE IRA is that the latter allows employees to also make contributions to their retirement savings. As a result, this option is likely best suited for small business owners with fewer than 100 employees.

With SIMPLE IRAs, business owners are required to contribute a certain percentage to their employees’ accounts. This includes making matching contributions of up to 3% of compensation and contributing at least 2% of compensation to all eligible employees regardless of whether they choose to contribute themselves. Additionally, like with SEP-IRAs, employees are always 100% vested. As for limits, employee contributions cannot exceed $13,500 a year for tax years 2020 and 2021. For the record, these employee contributions are also eligible for the aforementioned saver’s credit if applicable.

One more thing…

While we’re on the subject of taxes and retirement savings, it should be noted that — with the possible exception of Roth IRAs — taking early distributions from any of these account options could have some severely negative tax effects. For one, you’ll need to pay regular taxes on any distributions you take from your account regardless of your age. Additionally, those under 59 1/2 who take distributions will be assessed a 10% penalty on that money. Because of this, it’s never a good idea to take money from your retirement account before you actually retire (while not a great option, 401(k) loans are typically less costly than distributions in emergency situations).

Like I mentioned, the exception to this rule is Roth IRAs. Since you pay taxes up front, you can take distributions on your contributions without penalty. That said, this is still not a smart move and touching your gains will cost you as well. In all, it’s just one more thing to think about when decided which retirement savings option is right for you.

Even though Tax Day 2021 has been delayed a bit, it’s still just around the corner. Thus, now is the perfect time to consider your retirement savings options. In fact, in some cases, there may still be time to take advantage of the tax benefits these accounts offer in a bid to reduce your 2020 tax bill. Even if it’s too late for you this time, take this opportunity to not only plan for next year’s taxes but to also set yourself up for a comfortable and happy retirement — even if it does feel like forever from now.