Every now and then, I’ll come across a press release for a FinTech product that sounds pretty intriguing to me. When this happens, I’m usually pretty quick to do some research and see whether it’s worth reviewing for my weekly column on Dyer News or for my YouTube channel. However, in some cases, this extra bit of research reveals some dealbreakers that quickly dash my hopes. This happened a little over a year ago with the Binji card — and has now happened once again with the HMBradley rewards credit card.

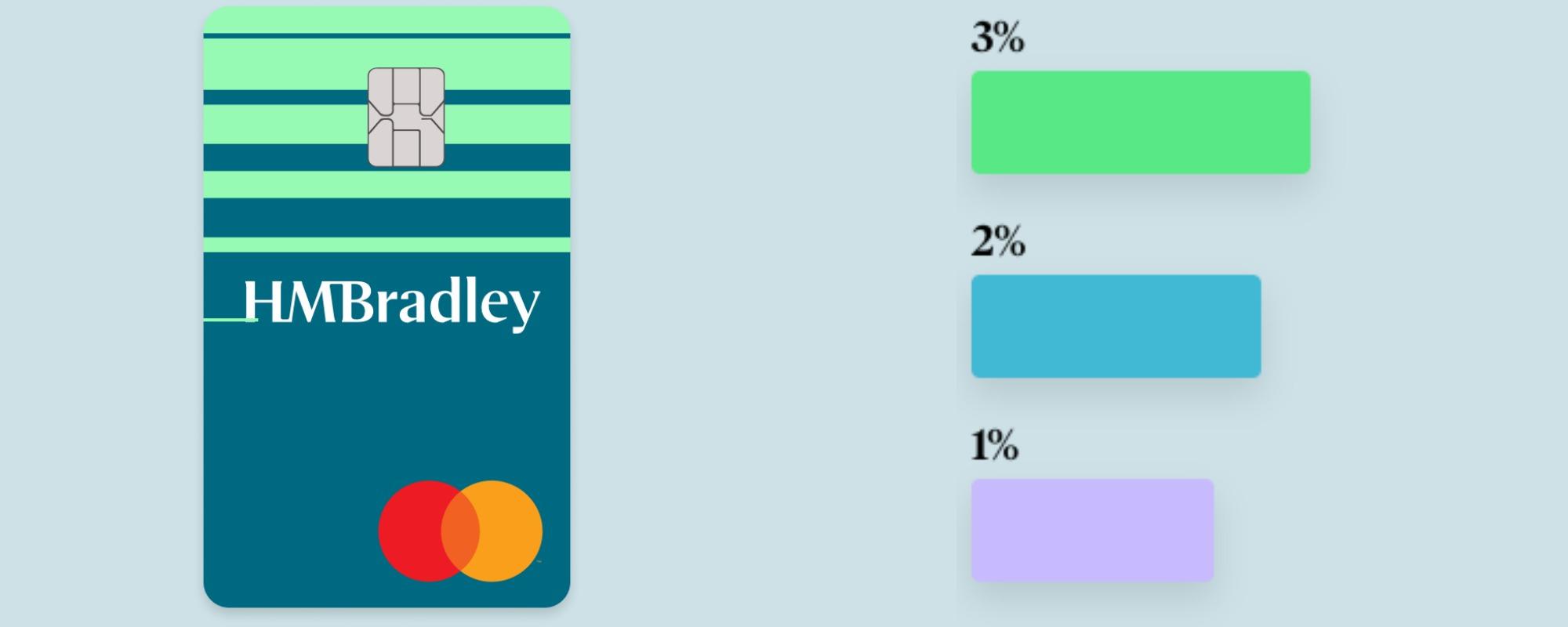

Before I get to the downsides, let me first explain what attracted me to the concept HMBradley announced this week. The new card will offer your typical 3%, 2% and 1% cashback categories, except that those top two slots won’t be the same for everyone. Instead, for each statement cycle, your purchases in your single largest spending category will yield you 3% back while purchases in your next largest category will earn you 2% and everything else gets you 1%.

To be sure, this arrangement isn’t completely unheard of, but it’s not exactly common among consumer credit cards. Moreover (lest credit card enthusiasts jump down my throat about this), with offerings such as the Citi Double Cash card already offering 2% back across the board, it’s really only that top multiplier that matters here. However, that’s where the Savings Tier component comes into play.

Another interesting aspect of HMBradley’s accounts is that users can currently earn up to 3% APY on their savings — which is all but unheard of these days thanks to the Fed slashing rates. In order to unlock this rate, however, users will need to save a significant portion of their direct deposits. Depending on their savings rate for the quarter, they can earn either 0.5%, 1%, 2%, or the aforementioned 3% APY. So what does this have to do with the new credit card? Well, those cardholders who spend at least $100 a month on their HMBradley rewards card will now get a boost up to the next highest Savings Tier. As a result, instead of needing to maintain a 20% savings rate in order to score that 3% APY, they’ll just need to set aside at least 15% (or as low as 10% to get 2% APY, etc.). Pretty cool, right?

Okay, so now for where this whole thing falls apart for me. First, as you may have caught in the previous paragraph, Savings Tiers are dependent on you making direct deposits to your HMBradley account. On that note, in order to qualify for the rewards card, you’ll need to make at least one direct deposit to your account per month as well as maintain an average balance of $250 or more. That’s not so bad for most people, but it makes a bit harder for me as a reviewer to go through the process. Alas, there’s yet another little catch I came across while digging into HMBradley’s FAQs: the credit card will carry a $60 annual fee. They do say that this will be waived for the first year, but that’s pretty significant regardless.

All things considered, I still think that HMBradley has some interesting ideas. And, to their credit, at least their loss-leading features already have some stipulations in place early instead of overhauling their platform down the road like many other FinTechs have. At the end of the day, while I can’t speak to the quality of HMBradley’s accounts, I could imagine someone utilizing their Savings Tiers and rewards credit card to come out on top. Nevertheless, catches such as the annual fee, balance requirements, and need for direct deposit make it less attractive to me (as both a reviewer and a customer). It’s just another reminder that it’s always worth doing a little extra research before jumping on something that seems like a slam dunk deal.