You may already know that Credit Utilization is the second-largest factor FICO considers when determining your credit score. Specifically, it makes up 30% of your score, topped only by Payment History at 35%. But what does that look like in practice? Well, I recently got the “opportunity” to see firsthand.

In April, I elected to pay a portion of my federal tax bill using my Capital One Venture card. FWIW, with Pay1040.com charging a 1.75% fee and the Venture card offering 2x back, this transaction was actually favorable to me. However, one downside is that, for whatever reason, the Capital One card has one of my lowest credit limits, coming in at just $5,000. And I decided to charge $4,200 to it (not to mention a few random purchases that were on it).

Rather than pay off this balance right away, I decided to let it linger until my actual payment due date. In turn, Capital One reported my card balance — and utilization — to the credit bureaus when my statement closed. That’s how I got to see what type of impact this would have.

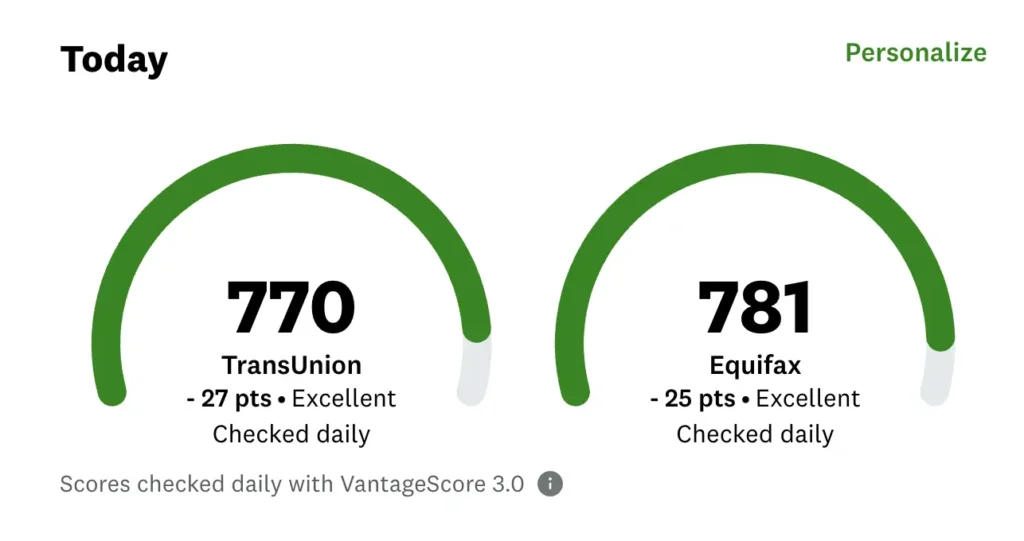

Prior to this experiment, I would have thought that your utilization would be calculated by considering all of your available credit versus your total balances. Yet, it seems pretty clear to me now that this is not the case. That’s because my near-maxed Venture card helped tank my score by more than 25 points! That’s a pretty sizable fall. In fact, it set off alarm bells for all of the credit monitoring apps I have, with each sending me push alerts and emails to make sure everything was okay.

Of course, the good news is that your credit score is just a snapshot in time. So, once I did pay off my balance and that statement was reported, my scores shot back up to where they were.

I should note for clarity that the scores I’m citing here come from Credit Karma, which utilizes VantageScore 3.0 models, not FICO. Still, I imagine that my “actual” scores experienced similar fluctuations during this time.

Also, I’m sharing this story not as a means of frightening you. As I stated, this ended up being a temporary blip in my score history — whereas something like a missed payment could haunt you far longer. Instead, I just think it’s interesting to see the real-world effects of these concepts we hear about so often. Plus, knowing how these things work can help you plan and prepare if you did need to apply for new credit and wanted your scores to look their best.

And there you have my “I Tanked My Credit Score for Science” post. I hope this gave you some new insight and helps you avoid making these types of mistakes at a time when they might actually matter.